Audit Planning:

Audit Mandate

- Audit of Missions/Posts, Tourism Offices, under section 13 and 16.

- Autonomous bodies, under section 20 (1).

- Units of PSUs, under section 19 (1).

- Audit of units of PSUs done on behalf of the Commercial Principal Auditors in India.

The Annual Audit Plan (AAP) for the respective years are being prepared on the basis of the information provided by the respective auditee entities and a comprehensive review of various risk parameters involving expenditure, revenue, staff strength, audit perception, etc.

In respect of overseas units of the PSUs, the data is sought from the erstwhile Member Audit Boards (MAB) offices, as they are the principal auditor of these PSUs. These commercial offices do the risk assessment of these units and send the audit proposal to IAO, London. Thereafter, these units are undertaken for audit along with the audits of the respective Missions/Posts.

Audit Execution

Audit Products:

The Audit products primarily associated with this office are Audit observations, LARs, Test Audit Notes, Management letters, Draft Paragraphs and Thematic Audits.

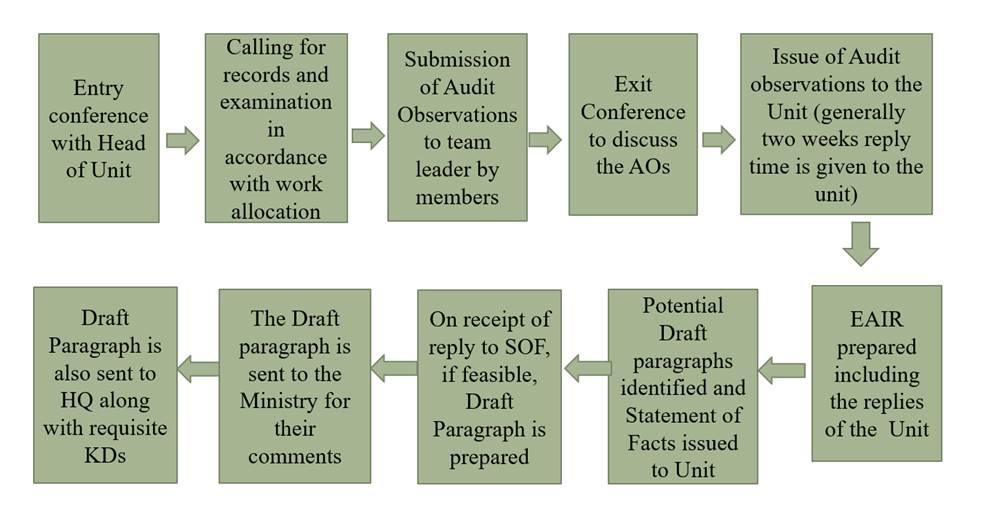

Consequent upon taking up the audit of a unit under jurisdiction, the office requisitions relevant records and documents. Thereafter, based upon the issues at hand and the replies of the auditee units thereon, a Local Audit Report (LAR) is issued to the auditee unit.

The important points noticed during audit are included in the Audit Reports relating to the Union Government. Para 5.3 and 5.4 of Union Government (Civil) Report No. 2 of 2021 are the recent contributions to the Audit Report which is accessible here

Audit Reporting:

The LAR is issued to the administrative Ministry, along with the auditee entity (Missions/Posts/PSUs/etc.). In respect of the overseas units of the PSUs, the LAR is issued to the unit and also reported to the Principal Auditor in IA&AD.

*EAIR may please be considered as LAR(Local Audit Report).